The following is the In the second quarter of 2022, the sales volume of China’s fast-moving consumer goods market increased by 2.8% year-on-year From CTR recommended by recordtrend.com. And this article belongs to the classification: CTR.

● the latest report released by the Kaidu consumer index (which is subordinate to CTR in China) shows that the sales of China’s fast-moving consumer goods market in the second quarter increased by 2.8% year-on-year, the same as the growth in the first quarter.

● under the influence of the epidemic, the growth driven categories of China’s FMCG market are quite different from last year. Food and household cleaning products were the main categories that drove the growth of the FMCG market in the second quarter, with sales growth of 9.5% and 5.7% respectively over the same period.

● influenced by the fact that consumers in some key cities are living at home, the development of beverages slowed down in the second quarter, with a year-on-year increase of only 1.2%. The downward pressure of personal care was more obvious, with a year-on-year decline of 4.4%.

● compared with the retail trend of social consumer goods in the second quarter released by the National Bureau of statistics, the development of the FMCG market is relatively stable, reflecting the resilience of people’s livelihood rigid demand categories.

● with Shanghai, Beijing and other major cities gradually returning to normal working and living conditions, the FMCG market rebounded rapidly in June, with a year-on-year increase of 5.2%. The resumption of work and production and the return of social activities have also led to a sharp rebound in beverages and personal care in the past four weeks.

● from the perspective of regional development, although the overall market rebounded rapidly in June, the growth in the eastern and northern regions has not recovered to the growth level before the outbreak in the first quarter of this year.

● relatively speaking, the southern and western regions less affected by the epidemic increased significantly in the second quarter, with sales rising by 4.4% and 2.8% year-on-year respectively.

● the performance of different channels continues to show obvious differentiation. Hypermarkets and supermarkets are still in a downward trend, while convenience stores and small supermarkets have entered a faster upward channel, meeting the convenience needs of consumers during the epidemic. Therefore, in the second quarter, convenience stores and small supermarkets increased by 13.8% and 11.4% respectively.

Increased competition from major retailers

Yonghui Wal Mart spar performs brilliantly

● under the background of continuous pressure on offline physical channels, the market share competition among major retailers is becoming increasingly fierce. Yonghui group is narrowing the share gap with Gaoxin retail group.

● Gaoxin retail, which is dominated by shopping malls, was significantly impacted by the epidemic in East China, and its market share fell by 0.8 percentage points year-on-year in the second quarter.

● Yonghui made progress in the strategic transformation of its Omni channel business. Bravo supermarket bucked the trend in the second quarter, and its sales increased by 7.4% year-on-year.

● this change also shows that consumers’ shopping habits have further evolved towards a faster, closer and easier consumption scenario.

Data source: Kaidu consumer index

● benefiting from the excellent performance of Sam’s club, Wal Mart’s overall market share continued to increase in the second quarter, surpassing China Resources Vanguard as the third largest retailer.

● the driving force of Sam’s club store’s adverse growth is mainly the continuous increase in customer penetration and the increase in purchase frequency, which also shows that the highly differentiated retail model will continue to increase its appeal to Chinese consumers with the support of supply chain and commodity advantages.

● the market share of spar system reached 2% in the second quarter, with a year-on-year increase of 0.3 percentage points. Guangdong Jiarong supermarket, a member of the system, accelerated the strategic layout of the four regions in the province and carried out the coordinated development of multiple formats. The penetration rate in the second quarter of this year increased by 0.4 percentage points year-on-year, constantly strengthening regional competitiveness.

● jiajiayue, a regional retail leader in Shandong, continued to maintain stable growth and entered a new discount store track, and its market share continued to increase in the second quarter.

Jd.com and interest e-commerce break through the growth dilemma

● among mainstream e-commerce platforms, jd.com continued to maintain a good momentum of consumer growth, with its penetration rate increasing by 0.8 percentage points in the second quarter, and maintained steady growth for three consecutive months.

● from April to June, the nationwide logistics sealing and control has a great impact on the performance of e-commerce. The accumulation of JD self support mode has solved the fragile supply chain problems under the epidemic, and also improved the continuous re purchase of loyal users and the continuous penetration of new categories.

● compared with last year, the penetration rate of Alibaba and pinduoduo decreased slightly in the second quarter.

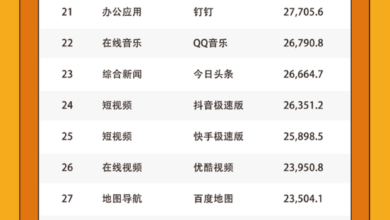

● during the period when consumers stayed at home in the second quarter, the short videos represented by Tiktok and Kwai received a lot of attention, and their penetration rate also increased by 9.3 and 2.3 percentage points respectively.

Data source: Kaidu consumer index

● 618 in 2022 is the first e-commerce shopping festival after the epidemic has stabilized, and has also received great attention from platforms and businesses, hoping to release the previously suppressed consumption enthusiasm due to logistics obstacles. Major platforms have increased subsidies to businesses and consumers, and the marketing nodes are more compact.

● however, due to the lack of anchor with goods on the head, e-commerce did not usher in the expected sharp consumption rebound. Compared with the same period in the first four weeks of June 17, 2022, the overall e-commerce channel increased by 7.5%, and beverages, food, and household cleaning products became the main commodity types of 618 this time.

Real time retail is attacking in the filling

● the epidemic has had a profound impact on the change of consumers’ purchasing behavior, and new models such as instant retail o2o have pushed consumers’ demand for convenience and freshness to a new height.

● in the continuous innovation and evolution, real-time retail delivery time is faster, the selection period is more flexible, and the goods available are more abundant, which promotes more new consumption scenarios, making consumers willing to spend more time through the real-time retail platform to meet the shopping mission different from the previous traditional supermarket, and also making the sales of real-time retail increase by 20% and 23% year-on-year in April and may 2022, respectively.

● the competition in the real-time retail market is becoming increasingly fierce, and the requirements of large-scale development also make this business form a winner take all pattern.

● in the community group purchase, the market share of meituan preferred and buy more vegetables has reached more than 80% in the second quarter, and JD home also occupies a greater advantage in the platform category.

● under the influence of the epidemic, compared with the second quarter of 2021, the penetration rate of community group buying increased the most, and consumers also continued to increase their spending in front warehouse retailers.

● Kaidu consumer index believes that the current first tier cities have led the growth of real-time retail. With the layout of this model in the country and the formation of consumers’ digital buying habits, real-time retail o2o will further improve the performance ability of offline physical stores and provide customers with a more convenient, efficient and high-quality real-time consumption experience.

More reading: CTR: a brief analysis of the TV viewing characteristics of young viewers in small and medium-sized cities CTR: TV advertising spending increased by 12.5% year-on-year in May 2021 CTR: overview of outdoor advertising data in May 2022 CTR: advertising market spending increased by 9.5% month on month in May 2022 CTR: radio advertising publishing costs fell by 4.4% year-on-year from January to April 2022 CTR: advertising market spending fell by 19.5% CTR: popular vertical app strength list in April 2022 CTR: Radio and television in the first quarter of 2022 The cost of advertising and publication increased slightly by 0.7% year on year CTR: the cost of traditional outdoor advertising and publication fell by 33.7% year on year in December 2021 CTR: the cost of TV advertising and publication increased by 9.9% month on month in December 2021 CTR: the official list of short videos of banking institutions in December 2021 CTR: 2021 China’s advertising market trends (with download) CTR: Q2 Internet TV media analysis report in 2021 CTR: in October 2021, the cost of TV advertising cases decreased by 12.3% year-on-year, with a slight decrease of 0.1% month on month. CTR: in October 2021, the cost of traditional outdoor advertising cases decreased by 21.3% year-on-year, and increased by 2.6% month on month

If you want to get the full report, you can contact us by leaving us the comment. If you think the information here might be helpful to others, please actively share it. If you want others to see your attitude towards this report, please actively comment and discuss it. Please stay tuned to us, we will keep updating as much as possible to record future development trends.

RecordTrend.com is a website that focuses on future technologies, markets and user trends. We are responsible for collecting the latest research data, authority data, industry research and analysis reports. We are committed to becoming a data and report sharing platform for professionals and decision makers. We look forward to working with you to record the development trends of today’s economy, technology, industrial chain and business model.Welcome to follow, comment and bookmark us, and hope to share the future with you, and look forward to your success with our help.