The following is the In 2020, the market scale of IT solutions in China’s banking industry reached 50.24 billion yuan, with a year-on-year increase of 18.0% From IDC recommended by recordtrend.com. And this article belongs to the classification: IDC.

In this context, IDC has been studying and tracking the market for 11 consecutive years. On September 7, 2021, IDC released the reports of China’s banking IT solutions market share, 2020 and China’s Insurance IT solutions market share, 2020. In the report, based on the research on the development of IT solution Market in China’s financial industry in 2020, IDC expounds the changes in the overall market environment, the needs of financial institutions, the main manufacturers and market competition pattern in different market segments, the development characteristics and trends of the industry, so as to comprehensively show the pattern and picture of the overall market, It can provide a reference for thinking about the key direction of digital transformation of financial institutions in the future, finding and analyzing the development status and potential of head financial technology manufacturers, and making an overall judgment on the market.

Observation on it solution market of China’s banking industry in 2020

In 2020, under the influence of various factors, the banking industry’s market demand for it solutions will show a relatively stable development trend. In the first half of 2020, the bank’s IT solution procurement and project promotion were delayed due to the impact of the epidemic, but in the second half of 2020, the demand for relevant orders increased significantly, and the digital transformation continued to advance.

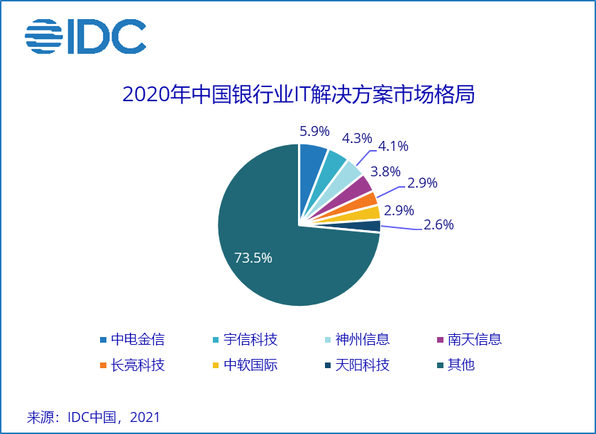

In 2020, the overall scale of China’s banking IT solution market will reach 50.24 billion yuan, an increase of 18.0% over 2019. IDC predicts that the average annual compound growth rate of the market from 2021 to 2025 will be 14.64%. IDC predicts that by 2025, the market scale of IT solutions in China’s banking industry will reach 118.56 billion yuan. From the perspective of competition pattern, manufacturers such as CLP Jinxin, Yuxin technology and Shenzhou information still maintain a leading position.

IDC research found that the overall banking IT solution market presents the following characteristics:

The upgrading of distributed core and the supporting transformation of peripheral systems are still the key areas invested by major banks. In the next five years, the market scale of Bank of China’s core business system will still maintain stable growth, and will show a rapid growth trend in the past two years. At present, the main driving factor comes from the host down construction in the distributed transformation; At the same time, the credit operating system has entered the update iteration window period. With the architecture of the distributed core system, the demand for Taihua reconstruction in the credit system has increased.

Strengthen the investment in data capacity-building to realize the fine operation and management of various businesses. Make use of big data, artificial intelligence, blockchain and other technologies to empower marketing, customer acquisition, risk control and other capabilities, improve the management, analysis and utilization level of data, and accelerate the construction of various business capabilities such as retail transformation and transaction banking.

Ecological scenario construction has been valued as an opportunity for banks to expand their outreach. Especially under the influence of the epidemic, the demand for ecological scene construction serving online channels has been stimulated. Banks actively explore more innovative service models and improve the level of open services.

It solution market observation of China’s insurance industry in 2020

In 2020, driven by a number of insurance regulatory policies, the impact and stimulation of the epidemic, the innovation demand for insurance business transformation and other factors, the investment in science and technology and the demand for science and technology services of insurance institutions will continue to grow. At present, China’s insurance density, insurance depth and the proportion of insurance assets in total financial assets still have a large gap compared with generally developed countries. It is necessary to accelerate the development and innovation of insurance business with the help of science and technology.

In 2020, the IT solution market of China’s insurance industry will continue to maintain a growth trend, with the market scale reaching RMB 12.14 billion, an increase of 18.2% compared with 2019. The overall market still maintains the characteristics of high concentration, and Zhongke soft still maintains a leading position in the whole market share.

IDC research found that the overall insurance it solution market presents the following characteristics:

· 1. The transformation of core business system is still the field with the highest proportion of investment. At present, insurance institutions usually tend to make use of the original technical basis as much as possible, improve the business support ability of the core system through appropriate and necessary transformation, and carry out distributed transformation and innovation construction suitable for different institutions on the premise of ensuring stability and security.

· 2. The investment in online capacity-building has received obvious attention. The agent’s ability of remote order issuing, remote exhibition, online sales and service is the focus of construction in 2020.

· 3. Strengthen the construction of data capacity. In 2020, insurance institutions began to increase the construction of underlying data capacity, strengthen data governance, and improve the efficiency and level of data quality, analysis and utilization, so as to support the standardized development and innovation of business.

Wang Chen, analyst of IDC’s China financial industry research department, said that in 2020, a series of supporting policies for financial science and technology, the reverse promotion of the epidemic, and the increasing maturity and improvement of technology applications provided a number of conditions for the continuous promotion of the overall market demand. After several years of digital transformation, financial institutions have made varying degrees of progress in core reconstruction, online channel construction, marketing customer acquisition and risk control. In 2021, financial institutions will continue to support business innovation and transformation through technological route transformation, focus on agility, remoteness, digitization and ecology, and continue to increase their commitment and intensity in it construction and transformation. Meanwhile, as financial technology subsidiaries and large cloud service providers continue to make efforts to enter the market, the competition and cooperation situation of the overall market may change in the future. Different types of manufacturers are expected to provide more comprehensive and innovative IT solutions for financial institutions by exploring new technology output modes in competition and cooperation.

More reading: IDC: in 2020, the overall scale of China’s banking IT solutions market reached 50.24 billion yuan IDC: in 2013, the overall scale of China’s banking IT solutions market was 14.825 billion yuan IDC: in 2013, the scale of China’s banking IT solutions market was 14.825 billion yuan IDC: in the second quarter of 2021, the global shipment of smart phones was 313 million, an increase of 13.2% IDC: It is estimated that in 2020, the shipment of second-hand smart phones will exceed 225 million, with a year-on-year increase of 9.2%. IDC: in 2020, the sales volume of the global wearable device market will reach 444.7 million, with a year-on-year increase of 28.4%. IDC: it is estimated that the global sales volume of smart phones in 2018 will be 1.462 billion. IDC: in Q2, Apple iPad shipped 12.9 million units, exceeding the sum of Samsung and Amazon. IDC: in 2016, the global total shipment of smart phones will be 1.47 billion, with a year-on-year increase of 2.3% : Q4 China’s media tablet device shipments reached 810000 units in 2010 IDC: Q3 Apple’s share in China fell below 10% in 2012 and ranked No. 6 IDC: Q3 Australia’s iPhone market share rose to 46.42% in 2016 IDC: Q2 Global Virtual Reality (VR) helmet shipments fell 33.7% year-on-year in 2018 IDC: 2014 supply chain strategy forecast IDC: Apple watch’s market share is expected to reach 27.5% in 2023

If you want to get the full report, you can contact us by leaving us the comment. If you think the information here might be helpful to others, please actively share it. If you want others to see your attitude towards this report, please actively comment and discuss it. Please stay tuned to us, we will keep updating as much as possible to record future development trends.

RecordTrend.com is a website that focuses on future technologies, markets and user trends. We are responsible for collecting the latest research data, authority data, industry research and analysis reports. We are committed to becoming a data and report sharing platform for professionals and decision makers. We look forward to working with you to record the development trends of today’s economy, technology, industrial chain and business model.Welcome to follow, comment and bookmark us, and hope to share the future with you, and look forward to your success with our help.

-

-

-

-